Spiralling memory spot prices could trigger 'industry cycle collapse,' report warns — NAND wafer costs surge 25% in a single month

Source: Tom’s Hardware

Image credit: Micron

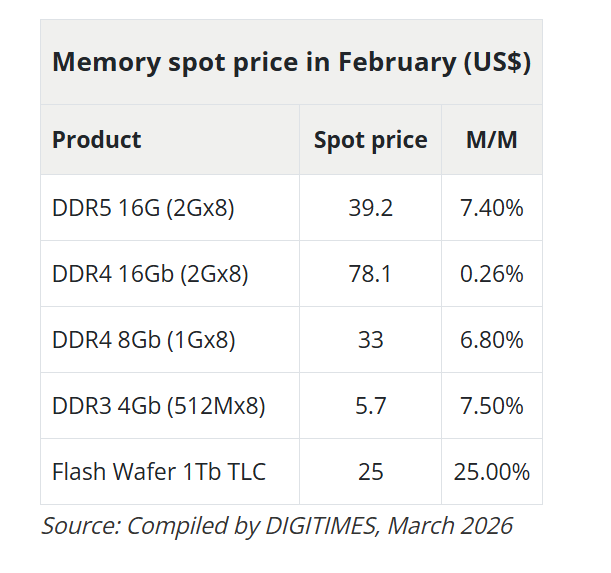

Memory spot prices rose broadly in February 2026, with NAND flash wafer costs leading the way, according to DigiTimes market data compiled this month. The report warns that the widening gap between demand and supply is driving rapid spot‑price increases and procurement‑capital pressures, which, if continued, could trigger an “industry cycle collapse.”

DRAM Spot Prices

- DDR4: Mixed results. The 16 Gb (2Gx8) variant held nearly flat, rising just 0.26 % to $78.10, while the 8 Gb (1Gx8) gained 6.8 % to $33.

- DDR3: 4 Gb (512Mx8) chips rose 7.5 % to $5.70.

The slower DDR4 gains reflect a moderation from the 20–30 % monthly increases seen across DRAM products in January. DigiTimes notes this pullback is “partly seasonal rather than a sign of easing structural pressure.”

Image credit: DigiTimes

Contract Price Outlook

The February spot data arrives amid sharply higher contract‑price forecasts:

- Conventional DRAM: TrendForce revised its Q1 2026 contract‑price outlook upward in early February, raising the estimate from a prior 55–60 % quarter‑over‑quarter increase to 90–95 %. PC DRAM is now projected to more than double quarter‑over‑quarter, a new quarterly record.

- NAND flash: Contract prices are forecast to rise 55–60 % QoQ, up from an earlier 33–38 % estimate.

Drivers of Demand

AI infrastructure continues to pull memory capacity toward server DRAM and high‑bandwidth memory, leaving conventional DRAM and consumer NAND segments undersupplied. North American cloud service providers have been pulling forward orders since late 2025, locking in allocations and pushing other buyers down the priority queue. TrendForce noted that even tier‑1 PC OEMs with secured supplier allocations have seen inventory levels decline.

NAND Flash Spot Prices

The February spot jump extends a troubling longer‑term trend. According to DigiTimes, citing ChinaFlashMarket data:

- 1 Tb QLC/TLC flash wafer prices have roughly tripled since October 2025.

- 512 Gb TLC prices are up nearly fivefold over the same period.

Suppliers are redirecting capacity toward enterprise SSDs—where margins are higher—limiting wafer availability for module makers and sustaining upward pressure across the category.